As filed with the United States Securities and Exchange Commission on February 1, 2021.

Registration Statement No. 333-252166

England and Wales | | | 2836 | | | Not applicable |

(State or other jurisdiction of incorporation or organization) | | | (Primary Standard Industrial Classification Code Number) | | | (I.R.S. Employer Identification Number) |

Divakar Gupta Eric W. Blanchard Peter Byrne Courtney T. Thorne Cooley LLP 55 Hudson Yards New York, New York 10001 +1 212 479 6000 | | | Nicola Maguire Claire Keast-Butler Thomas Goodman Cooley (UK) LLP Dashwood 69 Old Broad Street London EC2M 1QS United Kingdom +44 20 7583 4055 | | | Simon Witty Davis Polk & Wardwell London LLP 5 Aldermanbury Square London EC2V 7HR United Kingdom +44 20 7418 1300 | | | Richard D. Truesdell, Jr. Yasin Keshvargar Davis Polk & Wardwell LLP 450 Lexington Avenue New York, New York 10017 +1 212 450 4000 |

Title of Each Class of Securities to be Registered | | | Amount to be Registered(1) | | | Proposed Maximum Offering Price Per Share(2) | | | Proposed Maximum Aggregate Offering Price(1)(2) | | | Amount of Registration Fee(5) |

Ordinary shares, nominal value £0.002 per share(3)(4) | | | 9,583,332 | | | $25.00 | | | $239,583,300 | | | $26,139 |

(1) | Includes 1,249,999 shares that the underwriters have the option to purchase. |

(2) | Estimated solely for the purpose of calculating the registration fee in accordance with Rule 457(a) of the Securities Act of 1933, as amended. |

(3) | These ordinary shares are represented by ADSs, each of which represents one ordinary share of the Registrant. |

(4) | ADSs issuable upon deposit of the ordinary shares registered hereby are being registered pursuant to a separate registration statement on Form F-6 (File No. 333-252487). |

(5) | The registrant previously paid a registration fee of $10,910 in connection with the initial filing of this Registration Statement. |

1 | We have submitted an application to the Registrar of Companies in England and Wales for re-registration as a public limited company with the name Immunocore Holdings plc. |

† | The term “new or revised financial accounting standards” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. |

| | | PER ADS | | | TOTAL | |

Initial public offering price | | | $ | | | $ |

Underwriting discounts and commissions(1) | | | | | ||

Proceeds, before expenses, to us | | | | |

(1) | See “Underwriting” for additional information regarding total underwriter compensation. |

Goldman Sachs & Co. LLC | | | J.P. Morgan | | | Jefferies |

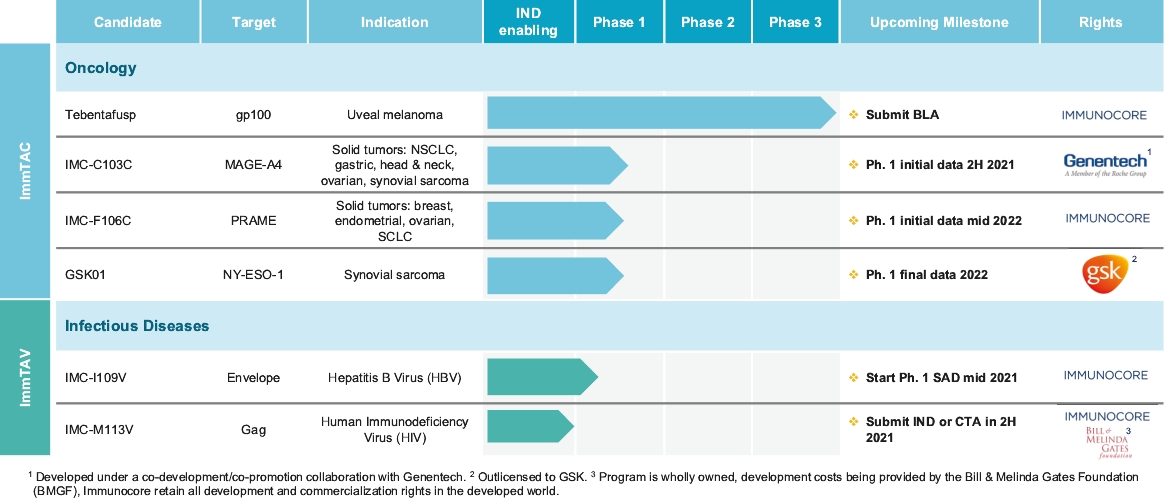

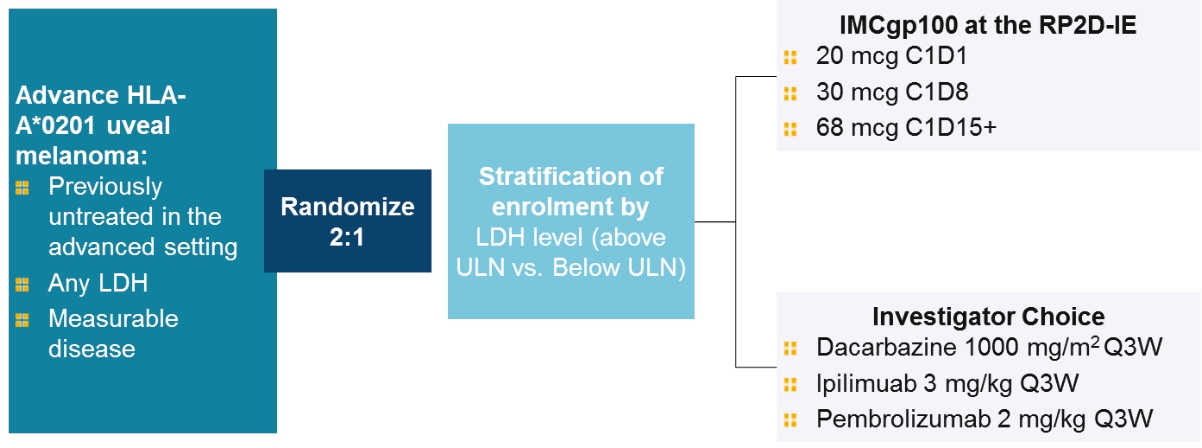

• | Tebentafusp, our ImmTAC molecule targeting an HLA-A*02:01 gp100 antigen, demonstrated monotherapy activity and recently achieved the primary endpoint of superior overall survival at the first pre-planned interim analysis of a randomized Phase 3 clinical trial in patients with previously untreated metastatic uveal melanoma. We anticipate submitting a BLA to the FDA in the third quarter of 2021 followed by a Marketing Authorization Application, or MAA, submission to the European Medicines Agency, or EMA. |

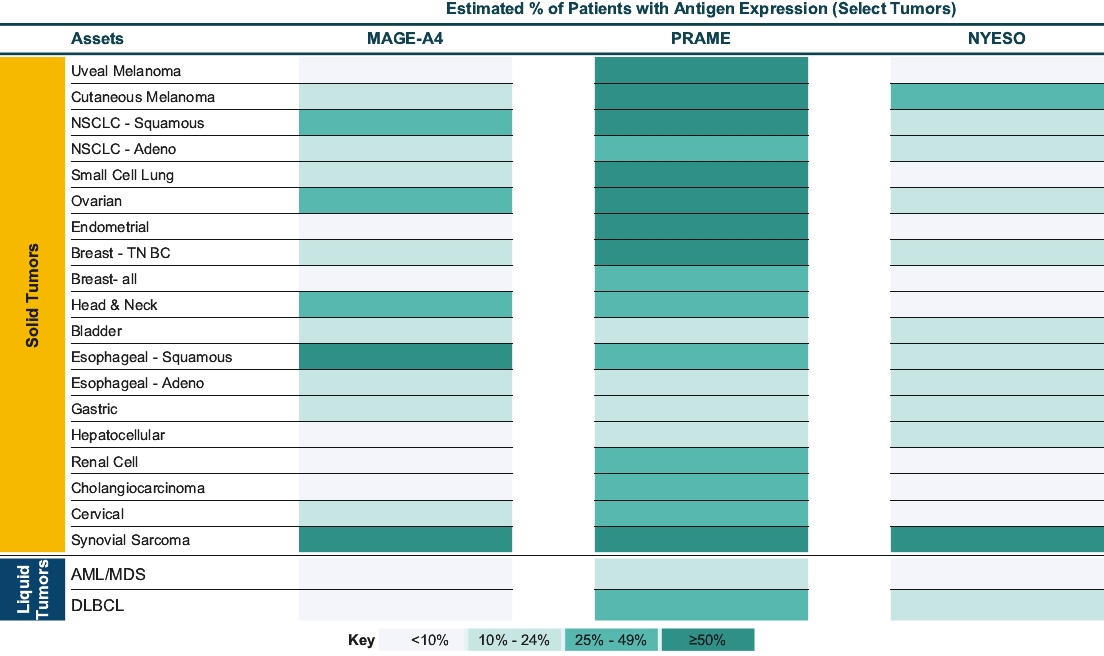

• | IMC-C103C, our ImmTAC molecule targeting an HLA-A*02:01 MAGE-A4 antigen, is currently being evaluated in a first-in-human, Phase 1/2 dose escalation trial in patients with solid tumor cancers including non-small-cell lung cancer, or NSCLC, gastric, head and neck, ovarian and synovial sarcoma. We believe this trial will demonstrate clinical activity of IMC-C103C, and we anticipate reporting Phase 1 initial data from this trial in the second half of 2021. We are developing this program under a co-development collaboration with Genentech, Inc., or Genentech, under which we have an option to retain 50% of the economics. |

• | IMC-F106C, our ImmTAC molecule targeting an optimal HLA-A*02:01 PRAME antigen identified with our MassSpec technology, is currently being evaluated in a first-in-human, Phase 1/2 dose escalation trial in patients with multiple solid tumor cancers including breast, endometrial, ovarian and small cell lung cancer, or SCLC. We believe this trial will demonstrate clinical activity of IMC-F106C, and we anticipate reporting Phase 1 initial data from this trial in mid-2022. |

• | GSK01, our ImmTAC molecule targeting an NY-ESO HLA-A*02:01 antigen, is currently being evaluated in the dose escalation phase of a Phase 1 clinical trial. When an optimal dosing regimen has been identified, a small expansion cohort of synovial sarcoma patients will be recruited to evaluate the clinical benefit of the therapeutic. This program is being developed under a collaboration with GlaxoSmithKline Intellectual Property Development Ltd, or GSK, which has an option to acquire full commercialization and development rights to this product candidate at the end of the ongoing Phase 1 clinical trial. |

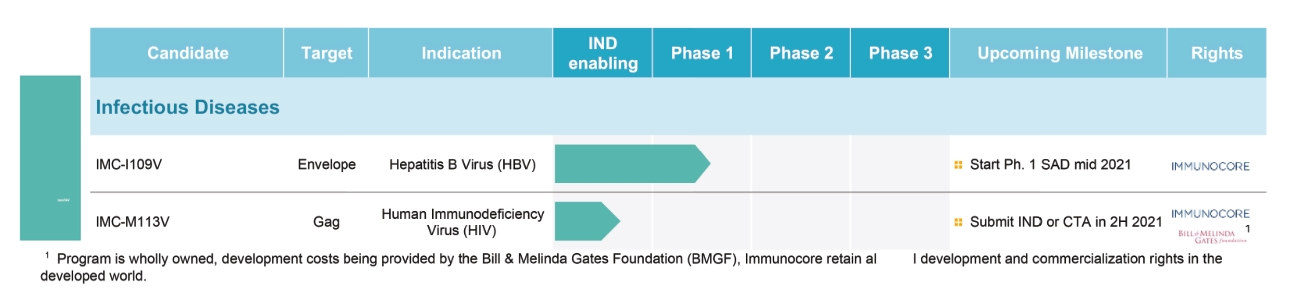

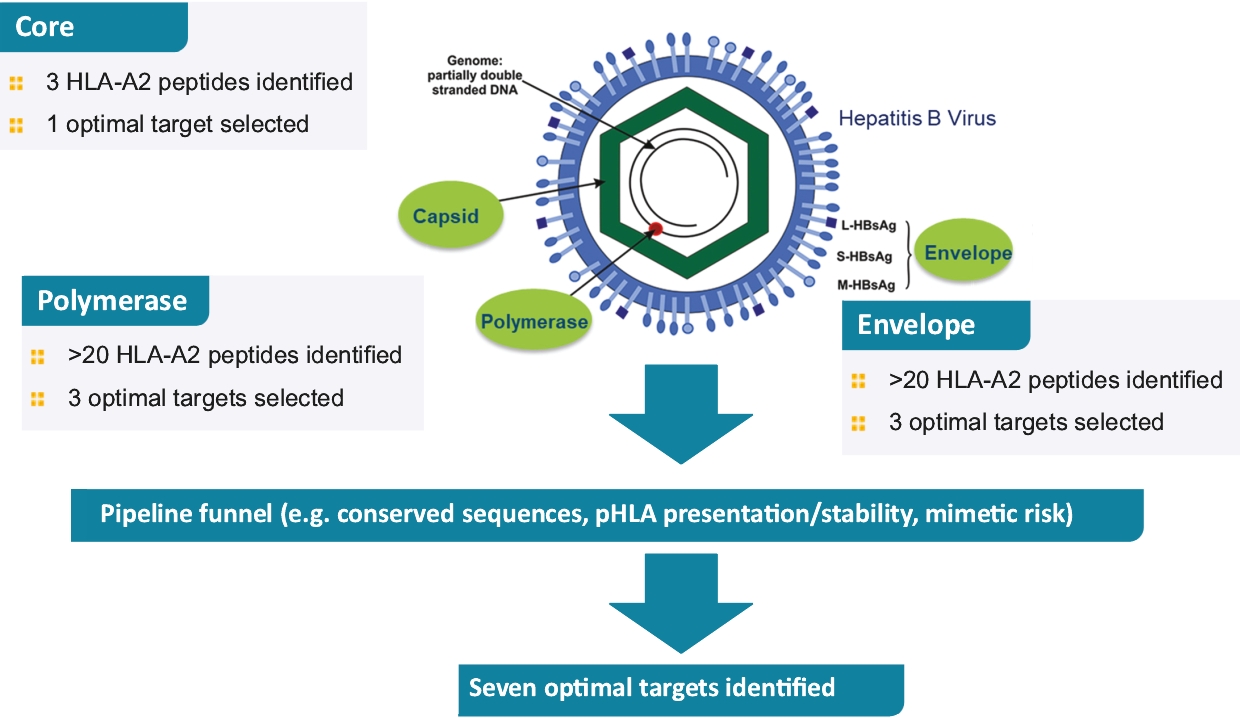

• | IMC-I109V, our ImmTAV molecule targeting a conserved HBV envelope antigen, is our most advanced ImmTAV program and is currently being evaluated in a Phase 1/2 clinical trial in patients with chronic HBV who are non-cirrhotic, hepatitis B e-Antigen negative, and virally suppressed on chronic nucleot(s)ide analogue therapy. Our goal is to develop a functional cure for HBV and we anticipate commencing dosing in our Phase 1 single ascending dose, or SAD, trial in mid-2021. We are also developing a next-generation version of this molecule leveraging our research into universal HLA-E molecules which could benefit a much larger patient population as compared to classical-HLA antigens. |

• | IMC-M113V, our ImmTAV molecule targeting an HIV gag antigen bispecific TCR molecule, is currently in pre-clinical development. Our HIV programs are funded by the Bill & Melinda Gates Foundation, or the Gates Foundation, and we are required to make any successfully approved products available at reduced prices in certain developing countries. We retain full development and commercial right in non-developing countries. |

• | Secure marketing approval for, and then commercialize, tebentafusp, our lead ImmTAC, for the treatment of metastatic uveal melanoma. |

• | Advance our IMC-C103C program targeting MAGE-A4 for the treatment of solid tumors in collaboration with Genentech. |

• | Advance our IMC-F106C program targeting PRAME for the treatment of solid tumors. |

• | Advance our IMC-I109V program for the treatment of chronic HBV. |

• | Continue to develop our novel universal ImmTAX platform to meaningfully broaden the eligible patient pool. |

• | Continue to invest in our platform to discover and develop novel therapeutics. |

• | Opportunistically pursue strategic partnerships to maximize the full potential of our pipeline and ImmTAX platform. |

• | We have incurred significant losses in every year since our inception. We expect to continue to incur losses over the next several years and may never achieve or maintain profitability. |

• | We will require substantial additional funding to achieve our business goals. If we are unable to obtain this funding when needed and on acceptable terms, we could be forced to delay, limit or terminate our product development efforts. |

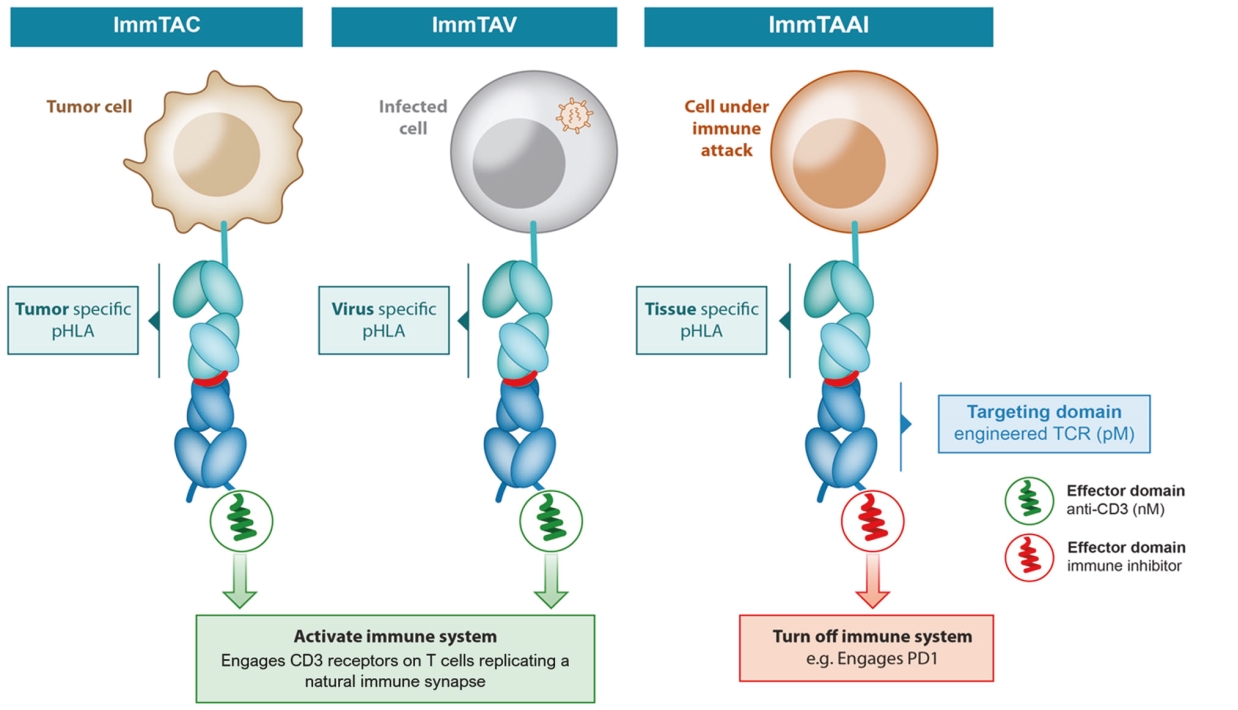

• | We are heavily dependent on the success of our ImmTAX platform to identify and develop product candidates. If we or our collaborators are unable to successfully develop and commercialize our platforms or experience significant delays in doing so, our business may be harmed. |

• | We may be unable to successfully complete additional large-scale, pivotal clinical trials for any product candidates we develop after tebentafusp. |

• | Our product candidates utilize a novel mechanism of action and involve novel targets which may result in greater research and development expenses, regulatory issues that could delay or prevent approval, or discovery of unknown or unanticipated adverse effects. |

• | Clinical product development involves a lengthy and expensive process, with an uncertain outcome. |

• | The effects of health epidemics, including the ongoing COVID-19 coronavirus pandemic, in regions where we, or the third parties on which we rely, have business operations could adversely impact our business, including our pre-clinical studies and clinical trials, as well as the business or operations of our CROs or other third parties with whom we conduct business. |

• | For a period of four weeks, our IMC-F106C program was put on partial clinical hold in 2020 by the FDA following the death of the second patient dosed in this trial, which was subsequently determined to be unrelated to study drug. The hold has since been lifted and the trial has been resumed. |

• | We are subject to manufacturing risks that could substantially increase our costs and limit supply of our products. |

• | We face substantial competition, which may result in others developing or commercializing drugs before or more successfully than us. |

• | Our existing collaborations are important to our business, and future collaborations may also be important to us. If we are unable to maintain any of these collaborations, or if these collaborations are not successful, our business could be adversely affected. |

• | If we are unable to adequately protect our proprietary technology or obtain, maintain, protect and enforce patent and other intellectual property protection for our technology and products or if the scope of the protection obtained is not sufficiently broad, our competitors and other third parties could develop and commercialize technology and products similar or identical to ours, and our ability to successfully commercialize our technology and products may be impaired. |

• | Third parties may initiate legal proceedings alleging that we are infringing, misappropriating or otherwise violating their intellectual property or proprietary rights, the outcome of which would be uncertain and could have a material adverse effect on the success of our business. |

• | The FDA regulatory pathways can be difficult to predict and whether, for example, further unanticipated clinical trials are required, will depend on the data obtained in our ongoing clinical trials. |

• | Our future success depends on our ability to retain key executives and experienced scientists and to attract, retain and motivate qualified personnel. |

• | As a company based outside of the United States, we are subject to economic, political, regulatory and other risks associated with international operations. |

• | We have identified a material weakness in our internal control over financial reporting and may identify material weaknesses in the future or otherwise fail to maintain proper and effective internal controls, which may impair our ability to produce timely and accurate financial statements or prevent fraud. If we are unable to establish and maintain effective internal controls, shareholders could lose confidence in our financial and other public reporting, which would harm our business and the trading price of our ADSs. |

• | an exemption from compliance with any requirement that the Public Company Accounting Oversight Board may adopt regarding mandatory audit firm rotation or a supplement to the auditor’s report providing additional information about the audit and the financial statements; |

• | reduced disclosure about our executive compensation arrangements; |

• | an exemption from the non-binding advisory votes on executive compensation, including golden parachute arrangements; and |

• | an exemption from the auditor attestation requirement in the assessment of our internal control over financial reporting pursuant to the Sarbanes-Oxley Act of 2002, or the Sarbanes-Oxley Act. |

• | to fund tebentafusp, our lead ImmTAC, for the treatment of metastatic uveal melanoma through the completion of our Phase 3 clinical trial as well as preparations for a commercial launch; |

• | to advance the clinical development of IMC-C103C targeting MAGE A4 for the treatment of solid tumors; |

• | to advance the clinical development of IMC-F106C targeting PRAME for the treatment of solid tumors; |

• | to advance the clinical development of IMC-I109V targeting a functional cure for chronic HBV; |

• | to continue to continue to advance our pre-clinical programs and invest in our ImmTAX platform to discover and develop novel therapeutic targets; and |

• | for working capital and general corporate purposes. |

• | 832,904 ordinary shares issuable upon the exercise of options outstanding under our existing equity incentive plans as of September 30, 2020, with a weighted-average exercise price of £63.23 per share (or $81.70 per share, based on the noon buying rate of the Federal Reserve Bank of New York on September 30, 2020, which was £1.00 to $1.2921); |

• | 5,706,279 ordinary shares reserved for future issuance under our 2021 Equity Incentive Plan, or the 2021 EIP, which will become effective in connection with this offering, as well as any automatic annual increases in the number of ordinary shares reserved for future issuance under the 2021 EIP, as more fully described in the section titled “Management—Equity Incentive Plans;” and |

• | 4,014,267 ordinary shares (assuming an initial public offering price of $24.00 per ADS, which is the midpoint of the price range set forth on the cover page of this prospectus) underlying the grants to be issued prior to the closing of this offering to certain of our officers, directors and employees under our 2021 EIP, contingent and effective upon the execution and delivery of the underwriting agreement relating to this offering, with an exercise price that is equal to or greater than the price per ADS at which our ADSs are first sold to the public in this offering. |

• | the completion of the transactions described in the section titled “Corporate Reorganization” prior to the completion of this offering, including (i) the 20 to 1 consolidation of all our ordinary shares and non-voting ordinary shares prior to completion of this offering, (ii) the re-designation of G1 shares held by our U.K. employees and former employees as deferred shares; (iii) 216,200 ordinary shares underlying the grants to be issued prior to the closing of this offering under our 2021 EIP (to our current employees) and under standalone option agreements (to our former employees) to replace the G1 shares that will be re-designated as deferred shares, conditional on and effective immediately prior to closing of this offering, with an exercise price that is equal to or greater than the price per ADS at which our ADSs are first sold to the public in this offering; (iv) the re-designation of G2 shares held by our U.K. employees into one ordinary share and three deferred shares, conditional on and effective immediately prior to closing of this offering; and (v) 96,300 ordinary shares underlying the grants to be issued prior to the closing of this offering under our 2021 EIP to replace the G2 shares that will be re-designated as a mixture of deferred shares and ordinary shares, conditional on and effective immediately prior to closing of this offering, with an exercise price that is equal to the price per ADS at which our ADSs are first sold to the public in this offering; |

• | an initial public offering price of $24.00 per ADS, which is the midpoint of the price range set forth on the cover page of this prospectus; and |

• | no exercise by the underwriters of their option to purchase up to 1,249,999 additional ADSs in this offering. |

| | | For the nine month period ended September 30, | | | For the year ended December 31, | |||||||

| | | 2020 | | | 2019 | | | 2019 | | | 2018 | |

| | | (pounds sterling, in thousands, except for share and per share data) | | | (pounds sterling, in thousands, except for share and per share data) | |||||||

Consolidated statement of loss and other comprehensive income data: | | | | | | | | | ||||

Revenue | | | 22,694 | | | 22,027 | | | 25,669 | | | 23,654 |

Other operating income | | | 408 | | | 420 | | | 185 | | | 622 |

Operating expenses: | | | | | | | | | ||||

Research and development | | | (57,566) | | | (75,415) | | | (99,991) | | | (83,575) |

Administrative expenses | | | (31,569) | | | (35,611) | | | (44,183) | | | (34,156) |

Operating loss | | | (66,033) | | | (90,579) | | | (118,320) | | | (93,455) |

Other income | | | — | | | — | | | — | | | 4,979 |

Finance income | | | 1,972 | | | 1,134 | | | 1,510 | | | 1,140 |

Finance costs | | | (2,272) | | | (6,532) | | | (9,379) | | | (842) |

Non-operating (expense) / income | | | (300) | | | (5,398) | | | (7,869) | | | 5,277 |

Loss before tax | | | (66,333) | | | (95,977) | | | (126,189) | | | (88,178) |

Income tax credit | | | 11,120 | | | 18,011 | | | 22,258 | | | 16,548 |

Loss for the period | | | (55,213) | | | (77,966) | | | (103,931) | | | (71,630) |

Exchange differences on translation of foreign operations | | | 338 | | | 82 | | | (99) | | | 72 |

Income tax effect relating to the components of other comprehensive income | | | — | | | — | | | — | | | 3,634 |

Total comprehensive loss for the period, net of tax | | | (54,875) | | | (77,884) | | | (104,030) | | | (67,924) |

| | ||||||||||||

Pro forma per share data:(1) | | | | | | | | | ||||

Basic and diluted loss per share(2) | | | (0.002) | | | (0.004) | | | (0.005) | | | (0.003) |

Basic and diluted weighted average number of shares | | | 27,306,935 | | | 21,579,880 | | | 22,297,935 | | | 21,558,890 |

| | | As of September 30, | | | As of December 31, | ||||

| | | 2020 | | | 2019 | | | 2018 | |

| | | (pounds sterling, in thousands) | | | (pounds sterling, in thousands) | ||||

Consolidated statement of financial position data: | | | | | | | |||

Cash and cash equivalents(3) | | | 56,687 | | | 73,966 | | | 124,385 |

Working capital(4) | | | 29,335 | | | 39,768 | | | 121,574 |

Total assets | | | 130,839 | | | 185,649 | | | 195,777 |

Interest-bearing loans and borrowings(3) | | | — | | | 19,157 | | | 18,878 |

Total liabilities(2) | | | 115,291 | | | 170,878 | | | 139,195 |

Share capital | | | 1 | | | — | | | — |

Total equity | | | 15,548 | | | 14,771 | | | 56,582 |

(1) | The unaudited pro forma loss per share data gives effect to our corporate reorganization. |

(2) | See Note 10 to our audited consolidated financial statements for the year ended December 31, 2019 and year ended December 31, 2018 and Note 6 to our unaudited consolidated financial statements appearing elsewhere in this prospectus for a description of the method used to compute diluted net loss per share. |

(3) | Excludes the borrowing of $50.0 million in November 2020 under a new debt facility with Oxford Finance Luxembourg S.A.R.L. |

(4) | We define working capital as current assets less current liabilities. |

• | continue our ongoing and planned development of our five clinical stage programs, including tebentafusp, our lead oncology program, which is being evaluated in a Phase 3 pivotal trial in patients with metastatic uveal melanoma; |

• | initiate pre-clinical studies and clinical trials for any additional product candidates that we may pursue in the future, including our earlier-stage programs; |

• | seek regulatory approvals for tebentafusp and any future product candidates that successfully complete clinical trials; |

• | build a portfolio of product candidates through the discovery, development, or acquisition or in-license of drugs, product candidates or technologies; |

• | establish a sales, marketing, manufacturing and distribution capability to commercialize tebentafusp and any future product candidate for which we may obtain marketing approval; |

• | maintain, protect, enforce and expand our intellectual property portfolio; |

• | acquire or in-license other product candidates, intellectual property and technologies; |

• | hire additional clinical, regulatory and scientific personnel; |

• | add operational, financial and management information systems and personnel, including personnel to support our product development and planned future commercialization efforts; and |

• | incur additional legal, accounting and other expenses associated with operating as a public company. |

• | progress, timing, scope and costs of our clinical trials, including the ability to timely initiate clinical sites, enroll subjects and manufacture soluble bispecific TCR product candidates for our ongoing, |

• | time and costs required to perform research and development to identify and characterize new product candidates from our research programs; |

• | the time and cost necessary to pursue regulatory authorizations and approvals that may be required by regulatory authorities to execute clinical trials or commercialize our products; |

• | our ability to successfully commercialize our product candidates, if approved; |

• | our ability to have clinical and commercial products successfully manufactured consistent with FDA, EMA and other authorities’ regulations; |

• | amount of sales and other revenues from product candidates that we may commercialize, if any, including the selling prices for such potential products and the availability of adequate third-party coverage and reimbursement for patients; |

• | sales and marketing costs associated with commercializing our products, if approved, including the cost and timing of building our marketing and sales capabilities; |

• | cost of building, staffing and validating our manufacturing processes, which may include capital expenditure; |

• | terms and timing of any revenue from our existing collaborations; |

• | costs of operating as a public company; |

• | time and cost necessary to respond to technological, regulatory, political and market developments; |

• | costs of filing, prosecuting, defending and enforcing any patent claims and other intellectual property rights; |

• | costs, associated with, and terms and timing of, any future any potential acquisitions, strategic collaborations, licensing agreements or other arrangements that we may establish; and |

• | inability of clinical sites to enroll patients as healthcare capacities are required to cope with natural disasters, epidemics or other health system emergencies, such as the COVID-19 pandemic. |

• | be delayed in obtaining marketing approval for our product candidates; |

• | not obtain marketing approval at all; |

• | obtain approval for indications or patient populations that are not as broad as intended or desired; |

• | be subject to post-marketing testing requirements; or |

• | have the product removed from the market after obtaining marketing approval. |

• | the research methodology used may not be successful in identifying potential indications and/or product candidates; |

• | potential product candidates may, after further study, be shown to have harmful adverse effects or other characteristics that indicate they are unlikely to be effective products; or |

• | it may take greater human and financial resources than we will possess to identify additional therapeutic opportunities for our product candidates or to develop suitable potential product candidates through internal research programs, thereby limiting our ability to develop, diversify and expand our product portfolio. |

• | delays or difficulties in enrolling and retaining patients in our clinical trials, including patients that may not be able or willing to comply with clinical trial protocols such as weekly dosing regimens if quarantines impede patient movement or interrupt healthcare services; |

• | delays or difficulties in clinical site initiation, including difficulties in recruiting and retaining clinical site investigators and clinical site staff; |

• | increased rates of patients withdrawing from our clinical trials following enrollment as a result of risks of exposure to COVID-19, being forced to quarantine or being unable to visit clinical trial locations or otherwise comply with clinical trial protocols; |

• | diversion or prioritization of healthcare resources away from the conduct of clinical trials and towards the COVID-19 pandemic, including the diversion of hospitals serving as our clinical trial sites and hospital staff supporting the conduct of our clinical trials, and because, who, as healthcare providers, may have heightened exposure to COVID-19 and adversely impact our clinical trial operations; |

• | interruption of our clinical supply chain or key clinical trial activities, such as clinical trial site monitoring, due to limitations on travel imposed or recommended by federal, state/provincial or municipal governments, employers and others; and |

• | limitations in employee resources that would otherwise be focused on the conduct of our clinical trials, including because of sickness of employees or their families or the desire of employees to avoid contact with large groups of people. |

• | delays in receiving approval from local regulatory authorities to initiate our planned clinical trials; |

• | delays in clinical sites receiving the supplies and materials needed to conduct our clinical trials; |

• | interruption in global shipping that may affect the transport of clinical trial materials, such as investigational drug product and comparator drugs used in our clinical trials; |

• | changes in federal, state/provincial or municipal regulations as part of a response to the COVID-19 coronavirus outbreak which may require us to change the ways in which our clinical trials are conducted, which may result in unexpected costs, or to discontinue the clinical trials altogether; |

• | delays in necessary interactions with local regulators, ethics committees and other important agencies and contractors due to limitations in employee resources or forced furlough of government employees; and |

• | the refusal of the FDA to accept data from clinical trials in these affected geographies. |

• | the FDA, EMA or comparable foreign regulatory authorities may disagree with the design or implementation of our clinical trials; |

• | the FDA, EMA or comparable foreign regulatory authorities may disagree with the design or implementation of our clinical trials; |

• | we may be unable to demonstrate to the satisfaction of the FDA, EMA or comparable foreign regulatory authorities that a product candidate is safe and effective for its proposed indication or a related companion diagnostic is suitable to identify appropriate patient populations; |

• | the results of clinical trials may not meet the level of statistical significance required by the FDA, EMA or comparable foreign regulatory authorities for approval; |

• | we may be unable to demonstrate that a product candidate’s clinical and other benefits outweigh its safety risks; |

• | the FDA, EMA or comparable foreign regulatory authorities may disagree with our interpretation of data from pre-clinical studies or clinical trials; |

• | the data collected from clinical trials of our product candidates may not be sufficient to support the submission a BLA or other submission or to obtain regulatory approval in the United States or elsewhere; |

• | the FDA, EMA or comparable foreign regulatory authorities may find deficiencies with or fail to approve the manufacturing processes or facilities of third-party manufacturers with which we contract for clinical and commercial supplies; and |

• | the approval policies or regulations of the FDA, EMA or comparable foreign regulatory authorities may significantly change such that our clinical data are insufficient for approval. |

• | regulators or institutional review boards, or IRBs, or ethics committees may not authorize us or our investigators to commence a clinical trial or conduct a clinical trial at a prospective trial site; |

• | we may experience delays in reaching, or fail to reach, agreement on acceptable terms with prospective trial sites and prospective CROs, the terms of which can be subject to extensive negotiation and may vary significantly among different CROs and trial sites; |

• | clinical trials of our product candidates may produce negative or inconclusive results, and we may decide, or regulators may require us, to conduct additional pre-clinical studies or clinical trials or we may decide to abandon product development programs; |

• | the number of patients required for clinical trials of our product candidates may be larger than we anticipate, enrollment in these clinical trials may be slower than we anticipate or participants may drop out of these clinical trials or fail to return for post-treatment follow-up at a higher rate than we anticipate; |

• | our third-party contractors may fail to comply with regulatory requirements or meet their contractual obligations to us in a timely manner, or at all, or may deviate from the clinical trial protocol or drop out of the trial, which may require that we add new clinical trial sites or investigators; |

• | we may elect to, or regulators or IRBs or ethics committees may require us or our investigators to, suspend or terminate clinical research for various reasons, including noncompliance with regulatory requirements or a finding that the participants are being exposed to unacceptable health risks; |

• | the cost of clinical trials of our product candidates may be greater than we anticipate; |

• | the supply or quality of our product candidates or other materials necessary to conduct clinical trials of our product candidates may be insufficient or inadequate; and |

• | our product candidates may have undesirable side effects or other unexpected characteristics, causing us or our investigators, regulators or IRBs or ethics committees to suspend or terminate the trials, or reports may arise from pre-clinical or clinical testing of other cancer therapies that raise safety or efficacy concerns about our product candidates. |

• | the severity of the disease under investigation; |

• | the eligibility criteria for the clinical trial in question; |

• | the availability of an appropriate genomic screening test; |

• | the perceived risks and benefits of the product candidate under study; |

• | the efforts to facilitate timely enrollment in clinical trials; |

• | the patient referral practices of physicians; |

• | the ability to monitor patients adequately during and after treatment; |

• | the proximity and availability of clinical trial sites for prospective patients; and |

• | factors we may not be able to control, such as current or potential pandemics that may limit patients, principal investigators or staff or clinical site availability (e.g., outbreak of COVID-19). |

• | our available capital resources or capital constraints we experience; |

• | the rate of progress, costs, and results of our clinical trials and research and development activities, including the extent of scheduling conflicts with participating clinicians and collaborators; |

• | our ability to identify and enroll patients who meet clinical trial eligibility criteria; |

• | our receipt of approvals by the FDA, EMA and comparable foreign regulatory authorities, and the timing thereof; |

• | other actions, decisions, or rules issued by regulators; |

• | our ability to access sufficient, reliable, and affordable supplies of materials used in the manufacture of our product candidates; |

• | our ability to manufacture and supply clinical trial materials to our clinical sites on a timely basis; |

• | the efforts of our collaborators with respect to the commercialization of our approved products, if any; and |

• | the securing of, costs related to, and timing issues associated with, commercial product manufacturing, as well as sales and marketing activities. |

• | differing regulatory requirements in foreign countries; |

• | unexpected changes in tariffs, trade barriers, price and exchange controls and other regulatory requirements; |

• | differing standards for the conduct of clinical trials; |

• | increased difficulties in managing the logistics and transportation of storing and shipping product candidates produced in the United States or elsewhere and shipping the product candidate to patients in other countries; |

• | import and export requirements and restrictions; |

• | economic weakness, including inflation, or political instability in foreign economies and markets; |

• | compliance with tax, employment, immigration and labor laws for employees living or traveling abroad; |

• | foreign taxes, including withholding of payroll taxes; |

• | foreign currency fluctuations, which could result in increased operating expenses and reduced revenue, and other obligations incident to doing business in another country; |

• | difficulties staffing and managing foreign operations; |

• | workforce uncertainty in countries where labor unrest is more common than in the United Kingdom or the United States; |

• | differing payor reimbursement regimes, governmental payors or patient self-pay systems, and price controls; |

• | potential liability under the Foreign Corrupt Practices Act of 1977, as amended, the U.K. Bribery Act 2010, or comparable foreign regulations; |

• | challenges enforcing or protecting our contractual and intellectual property rights, especially in those foreign countries that do not respect and protect intellectual property rights to the same extent as the United States or the United Kingdom; |

• | the impacts Brexit may have with respect to the cross-border acknowledgment of clinical trial results and marketing authorizations as well as recruitment of scientific personnel; |

• | production shortages resulting from any events affecting raw material supply or manufacturing capabilities abroad; and |

• | business interruptions resulting from geo-political actions, including war and terrorism. |

• | the inability to recruit, train and retain adequate numbers of effective sales and marketing personnel; |

• | the inability of sales personnel to obtain access to physicians or persuade adequate numbers of physicians to prescribe any future product that we may develop; |

• | the lack of complementary treatments to be offered by sales personnel, which may put us at a competitive disadvantage relative to companies with more extensive product lines; and |

• | unforeseen costs and expenses associated with creating an independent sales and marketing organization. |

• | the clinical indications for which our product candidates are approved; |

• | physicians, hospitals, cancer treatment centers, and patients considering our product candidates as a safe and effective treatment; |

• | hospitals and cancer treatment centers establishing the infrastructure required for the administration of the product candidate; |

• | the potential and perceived advantages of our product candidates over alternative treatments; |

• | the prevalence and severity of any side effects; |

• | product labeling or product insert requirements of the FDA, the EMA or other regulatory authorities; |

• | limitations or warnings contained in the labeling approved by the FDA or the EMA; |

• | the timing of market introduction of our product candidates as well as competitive products; |

• | the cost of treatment in relation to alternative treatments; |

• | the amount of upfront costs or training required for physicians to administer our product candidates; |

• | the pricing of our products and the availability of coverage and adequate reimbursement by third-party payors and government authorities; |

• | the willingness of patients to pay out-of-pocket in the absence of comprehensive coverage and adequate reimbursement by third-party payors and government authorities; |

• | relative convenience and ease of administration, including as compared to alternative treatments and competitive therapies; and |

• | the effectiveness of our sales and marketing efforts and distribution support. |

• | the impairment of our business reputation; |

• | the withdrawal of clinical trial participants; |

• | costs due to related litigation; |

• | the distraction of management’s attention from our primary business; |

• | substantial monetary awards to patients or other claimants; |

• | the inability to commercialize our product candidates; and |

• | decreased demand for our product candidates, if approved for commercial sale. |

• | collaborators have significant discretion in determining the efforts and resources that they will apply to these collaborations; |

• | collaborators may not perform their obligations as expected; |

• | collaborators may not pursue development and commercialization of any product candidates that achieve regulatory approval or may elect not to continue or renew development or commercialization programs based on clinical trial results, changes in the collaborators’ strategic focus or available funding, or external factors, such as an acquisition, that divert resources or create competing priorities; |

• | collaborators may delay clinical trials, provide insufficient funding for a clinical trial program, stop a clinical trial or abandon a product candidate, repeat or conduct new clinical trials or require a new formulation of a product candidate for clinical testing; |

• | collaborators could independently develop, or develop with third parties, products that compete directly or indirectly with our products or product candidates if the collaborators believe that competitive products are more likely to be successfully developed or can be commercialized under terms that are more economically attractive than ours; this may also happen if the collaborators’ development of competing products is substantially faster than our development timelines; |

• | collaborators may not further develop product candidates developed by us or co-developed with us under the collaboration; |

• | product candidates discovered in collaboration with us may be viewed by our collaborators as competitive with their own product candidates or products, which may cause collaborators to cease to devote resources to the commercialization of our product candidates; |

• | a collaborator with marketing and distribution rights to one or more of our product candidates that achieve regulatory approval may not commit sufficient resources to the marketing and distribution of such product or products; |

• | disagreements with collaborators, including disagreements over proprietary rights, contract interpretation or the preferred course of development, might cause delays or termination of the research, development or commercialization of product candidates, might lead to additional responsibilities for us with respect to product candidates, or might result in litigation or arbitration, any of which would be time-consuming and expensive; |

• | collaborators have certain defined rights to change or expand the scope of development programs during the course of the collaboration. This may lead to additional research work for us that may be time-consuming and expensive. Such work may compete with our own development programs and may delay timelines to market or proof-of-concept for our product candidates. If development programs under the collaboration turn out to be more costly and time-consuming, such unanticipated costs and work could likewise compete with our internal development programs; |

• | collaborators may not properly maintain, enforce or defend our intellectual property or proprietary information or may use them in such a way as to invite litigation that could jeopardize or invalidate our intellectual property or proprietary information or expose us to potential litigation; |

• | collaborators may infringe, misappropriate or otherwise violate the intellectual property or proprietary rights of third parties, which may expose us to litigation and potential liability, and collaborators may also allege that we are liable for potential infringement, misappropriation or other violations of third-party intellectual property or proprietary rights during the research and development work for the collaboration; |

• | certain collaborations may be terminated for the convenience of the collaborator and, if terminated, we could be required to raise additional capital to pursue further development or commercialization of the applicable product candidates. For example, certain of our collaboration and license agreements may be terminated for convenience upon the completion of a specified notice period; and |

• | collaborators may discontinue the development of product candidates within the collaboration, for example if they consider the results achieved so far or the product candidates not promising enough or if their development strategies change. |

• | have staffing difficulties; |

• | fail to comply with contractual obligations; |

• | experience regulatory compliance issues; |

• | undergo changes in priorities or become financially distressed; or |

• | form relationships with other entities, some of which may be our competitors. |

• | reliance on the third party for regulatory compliance and quality assurance; |

• | the possible breach of the manufacturing agreement by the third party; |

• | the possible misappropriation or unauthorized disclosure of our proprietary information, including our trade secrets and know-how; and |

• | the possible termination or nonrenewal of the agreement by the third party at a time that is costly or inconvenient for us. |

• | the scope of rights granted under the agreement and other interpretation-related issues; |

• | the extent to which our technology and processes infringe on intellectual property of the counterparty that is not subject to the agreement; |

• | the sublicensing of patent and other intellectual or proprietary rights under our collaborative development relationships; |

• | our diligence obligations under the agreement and what activities satisfy those diligence obligations; |

• | the inventorship and ownership of inventions and know-how resulting from the joint creation or use of intellectual property by our counterparty and us and our partners; and |

• | the priority of invention of patented technology. |

• | others may be able to make products that are similar to our product candidates or utilize similar technology but that are not covered by the claims of the patents that we own or license now or in the future; |

• | we or our licensors or collaborators might not have been the first to make the inventions covered by the issued patents or pending patent applications that we own or license now or in the future; |

• | we or our licensors or collaborators might not have been the first to file patent applications covering certain of our or their inventions; |

• | others may independently develop similar or alternative technologies or duplicate any of our technologies without infringing our intellectual property rights or any intellectual property rights we may license; |

• | it is possible that our present or future pending patent applications (whether owned or licensed) will not lead to issued patents; |

• | it is possible that there are or will be prior public disclosures that could invalidate our or our licensors’ or collaboration partners’ patents; |

• | issued patents that we hold rights to may fail to provide us with any competitive advantage, or may be held invalid or unenforceable, including as a result of legal challenges by our competitors or other third parties; |

• | our competitors or other third parties might conduct research and development activities in countries where we do not have patent rights or in countries where research and development safe harbor laws exist, and then use the information learned from such activities to develop competitive products for sale in our major commercial markets; |

• | we may not develop additional proprietary technologies that are patentable; |

• | the ownership, validity or enforceability of our patents or patent applications may be challenged by third parties; |

• | the patents or pending or future applications of others, if issued, may harm our business; and |

• | we may choose not to file a patent in order to maintain certain trade secrets or know-how, and a third party may subsequently file a patent covering such intellectual property. |

• | the FDA or comparable foreign regulatory authorities may disagree with the design or implementation of our or our collaborators’ clinical trials; |

• | we or our collaborators may be unable to demonstrate to the satisfaction of the FDA or comparable foreign regulatory authorities that our product candidates are safe, pure, potent and have a favorable risk/benefit profile for any of their proposed indications; |

• | the results of clinical trials may not meet the level of statistical significance required by the FDA or comparable foreign regulatory authorities for approval; |

• | the FDA or comparable foreign regulatory authorities may disagree with our interpretation of data from pre-clinical programs or clinical trials; |

• | data collected from clinical trials of product candidates may not be sufficient to the satisfaction of the FDA or comparable foreign regulatory authorities to support the submission of a BLA or other comparable submission in foreign jurisdictions or to obtain regulatory approval in the United States or elsewhere; |

• | the approval policies or regulations of the FDA or comparable foreign regulatory authorities may significantly change in a manner rendering our clinical data insufficient for approval. |

• | restrictions on the marketing or manufacturing of the product, withdrawal of the product from the market, or voluntary or mandatory product recalls; |

• | clinical trial holds; |

• | fines, warning letters or other regulatory enforcement action; |

• | refusal by the FDA to approve pending applications or supplements to approved applications filed by us; |

• | product seizure or detention, or refusal to permit the import or export of products; and |

• | injunctions or the imposition of civil or criminal penalties. |

• | the demand for our current or future product candidates, if we obtain regulatory approval; |

• | our ability to set a price that we believe is fair for our products; |

• | our ability to obtain coverage and adequate reimbursement for a product; |

• | our ability to generate revenue and achieve or maintain profitability; |

• | the level of taxes that we are required to pay; and |

• | the availability of capital. |

• | the federal Anti-Kickback Statute prohibits, among other things, persons from knowingly and willfully soliciting, offering, receiving or providing remuneration, directly or indirectly, in cash or in kind, to induce or reward either the referral of an individual for, or the purchase, order or recommendation of, any good or service, for which payment may be made under federal and state healthcare programs such as Medicare and Medicaid. A person or entity does not need to have actual knowledge of the statute or specific intent to violate it in order to have committed a violation; |

• | the federal civil and criminal false claims and civil monetary penalties laws, including the federal False Claims Act, or FCA, imposes criminal and civil penalties, including through civil whistleblower or qui tam actions, against individuals or entities for knowingly presenting, or causing to be presented, to the federal government, claims for payment that are false or fraudulent or making a false statement to avoid, decrease or conceal an obligation to pay money to the federal government. In addition, the government may assert that a claim including items and services resulting from a violation of the federal Anti-Kickback Statute constitutes a false of fraudulent claim for purposes of the False Claims Act; |

• | the federal Health Insurance Portability and Accountability Act of 1996, or HIPAA, imposes criminal and civil liability for executing a scheme to defraud any healthcare benefit program, or knowingly and willfully falsifying, concealing or covering up a material fact or making any materially false statement in connection with the delivery of or payment for healthcare benefits, items or services; similar to the federal Anti-Kickback Statute, a person or entity does not need to have actual knowledge of the statute or specific intent to violate it in order to have committed a violation; |

• | the federal physician payment transparency requirements, sometimes referred to as the “Sunshine Act” under the Affordable Care Act, require manufacturers of drugs, devices, biologics and medical supplies that are reimbursable under Medicare, Medicaid, or the Children’s Health Insurance Program to report to the Department of Health and Human Services information related to transfers of value made to physicians (currently defined to include doctors, dentists, optometrists, podiatrists and chiropractors) and teaching hospitals, as well as ownership and investment interests of such physicians and their immediate family members. Effective January 1, 2022, these reporting obligations will extend to include transfers of value made to certain non-physician providers including physician assistants, nurse practitioners, clinical nurse specialists, anesthesiologist assistants, certified registered nurse anesthetists and certified nurse midwives during the previous year; |

• | HIPAA, as amended by the Health Information Technology for Economic and Clinical Health Act of 2009 and its implementing regulations, impose obligations on certain covered entity healthcare providers, health plans, and healthcare clearinghouses as well as their business associates that perform certain services involving the use or disclosure of individually identifiable health information and their |

• | analogous state laws and regulations, such as state anti-kickback and false claims laws may apply to sales or marketing arrangements and claims involving healthcare items or services reimbursed by non-governmental third-party payors, including private insurers. Some state laws require pharmaceutical companies to comply with the pharmaceutical industry’s voluntary compliance guidelines and the relevant compliance guidance promulgated by the federal government in addition to requiring drug manufacturers to report information related to payments to physicians and other healthcare providers or marketing expenditures. Further, many state laws governing the privacy and security of health information in certain circumstances, differ from each other in significant ways and often are not preempted by HIPAA, thus complicating compliance efforts. |

• | convey, sell, lease, transfer, assign, dispose of or otherwise make cash payments consisting of all or any part of our business or property; |

• | effect certain changes in our business, management, ownership or business locations; |

• | merge or consolidate with, or acquire all or substantially all of the capital stock or assets of, any other company; |

• | create, incur, assume or be liable for any additional indebtedness, or create, incur, allow or permit to exist any additional liens; |

• | pay cash dividends on, make any other distributions in respect of, or redeem, retire or repurchase, any shares of our capital stock; |

• | make certain investments; and |

• | enter into transactions with our affiliates. |

• | increased operating expenses and cash requirements; |

• | the assumption of additional indebtedness or contingent liabilities; |

• | assimilation of operations, intellectual property and products of an acquired company or product, including difficulties associated with integrating new personnel; |

• | the diversion of our management’s attention from our existing product programs and initiatives in pursuing such a strategic merger or acquisition; |

• | retention of key employees, the loss of key personnel, and uncertainties in our ability to maintain key business relationships; |

• | risks and uncertainties associated with the other party to such a transaction, including the prospects of that party and their existing products or product candidates and regulatory approvals; and |

• | our inability to generate revenue from acquired technology and/or products sufficient to meet our objectives in undertaking the acquisition or even to offset the associated acquisition and maintenance costs. |

• | economic weakness, including inflation, or political instability in particular non-U.S. economies and markets; |

• | differing and changing regulatory requirements for product approvals; |

• | differing jurisdictions could present different issues for securing, maintaining or obtaining freedom to operate in such jurisdictions; |

• | potentially reduced protection for intellectual property and proprietary rights; |

• | difficulties in compliance with different, complex and changing laws, regulations and court systems of multiple jurisdictions and compliance with a wide variety of foreign laws, treaties and regulations; |

• | changes in non-U.S. regulations and customs, tariffs and trade barriers; |

• | changes in non-U.S. currency exchange rates of the pound sterling, U.S. dollar, euro and currency controls; |

• | changes in a specific country’s or region’s political or economic environment, including the implications of the recent decision of the United Kingdom to withdraw from the European Union; |

• | trade protection measures, import or export licensing requirements or other restrictive actions by governments; |

• | differing reimbursement regimes and price controls in certain non-U.S. markets; |

• | negative consequences from changes in tax laws; |

• | compliance with tax, employment, immigration and labor laws for employees living or traveling abroad, including, for example, the variable tax treatment in different jurisdictions of options granted under our share option schemes or equity incentive plans; |

• | workforce uncertainty in countries where labor unrest is more common than in the United States; |

• | litigation or administrative actions resulting from claims against us by current or former employees or consultants individually or as part of class actions, including claims of wrongful terminations, discrimination, misclassification or other violations of labor law or other alleged conduct; |

• | difficulties associated with staffing and managing international operations, including differing labor relations; |

• | production shortages resulting from any events affecting raw material supply or manufacturing capabilities abroad; and |

• | business interruptions resulting from geo-political actions, including war and terrorism, or natural disasters including earthquakes, typhoons, floods and fires. |

• | adverse results or delays in pre-clinical studies or clinical trials; |

• | reports of adverse events in products similar or perceived to be similar to those we are developing or clinical trials of such products; |

• | an inability to obtain additional funding; |

• | failure by us to successfully develop and commercialize our product candidates; |

• | failure by us to maintain our existing strategic collaborations or enter into new collaborations; |

• | failure by us to identify additional product candidates for our pipeline; |

• | failure by us or our licensors and strategic partners to prosecute, maintain, protect or enforce our intellectual property and proprietary rights; |

• | disputes or other developments relating to intellectual and other proprietary rights, including litigation |

• | matters and our ability to obtain patent and other intellectual property protection for our technologies; |

• | changes in laws or regulations applicable to future products; |

• | an inability to obtain adequate product supply for our product candidates or the inability to do so at acceptable prices; |

• | adverse regulatory decisions; |

• | the introduction of new products, services or technologies by our competitors; |

• | failure by us to meet or exceed financial projections we may provide to the public; |

• | failure by us to meet or exceed the financial projections of the investment community; |

• | the perception of the pharmaceutical industry by the public, legislatures, regulators and the investment community; |

• | changes in the structure of healthcare payment systems; |

• | announcements of significant acquisitions, strategic partnerships, joint ventures or capital commitments by us, our strategic partner or our competitors; |

• | additions or departures of key scientific or management personnel; |

• | significant lawsuits, including patent or shareholder litigation; |

• | changes in the market valuations of similar companies; |

• | general economic, industry, political and market conditions, including, but not limited to, the ongoing impact of the COVID-19 pandemic; |

• | sales of our ADSs or ordinary shares by us or our shareholders in the future; and |

• | the trading volume of our ADSs. |

• | delaying, deferring, or preventing a change in control; |

• | entrenching our management and/or the board of directors; |

• | impeding a merger, scheme of arrangement, takeover, or other business combination involving us; or |

• | discouraging a potential acquirer from making a takeover offer or otherwise attempting to obtain control of us. |

• | not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act, or Section 404; |

• | not being required to comply with any requirement that has or may be adopted by the Public Company Accounting Oversight Board regarding mandatory audit firm rotation or a supplement to the auditor’s report providing additional information about the audit and the financial statements; |

• | being permitted to provide only two years of audited financial statements in this initial registration statement, in addition to any required unaudited interim financial statements, with correspondingly reduced “Management’s Discussion and Analysis of Financial Condition and Results of Operations” disclosure; |

• | reduced disclosure obligations regarding executive compensation; and |

• | an exemption from the requirement to seek nonbinding advisory votes on executive compensation or golden parachute arrangements. |

• | In connection with a potential offer, if following an approach by or on behalf of a potential bidder, the company is “the subject of rumor or speculation” or there is an “untoward movement” in the company’s share price, there is a requirement for the potential bidder to make a public announcement about a potential offer for the company, or for the company to make a public announcement about its review of a potential offer. |

• | When a person or group of persons acting in concert (a) acquires, whether by a series of transactions over a period of time or not, interests in shares carrying 30% or more of the voting rights of a company (which percentage is treated by the Takeover Code as the level at which effective control is obtained) or (b) acquires an interest in any other shares which increases the percentage of shares carrying voting rights in which they are interested when they are already interested in shares which carry not less than 30% of the voting rights but do not hold shares carrying more than 50% of such voting rights, they must make a cash offer to all other shareholders at the highest price paid by them or any person acting in concert with them in the 12 months before the offer was announced. |

• | When interests in shares carrying 10% or more of the voting rights of a class have been acquired by an offeror (i.e., a bidder) and any person acting in concert with it in the offer period (i.e., before the shares subject to the offer have been acquired) or within the previous 12 months, the offer must be in cash or be accompanied by a cash alternative for all shareholders of that class at the highest price paid by the offeror or any person acting in concert with them in that period. Further, if an offeror or any person acting in concert with them acquires any interest in shares during the offer period, the offer for the shares must be in cash or accompanied by a cash alternative at a price at least equal to the price paid for such shares during the offer period. |

• | If after an announcement is made, the offeror or any person acting in concert with them acquires an interest in shares in an offeree company (i.e., a target) at a price higher than the value of the offer, the offer must be increased to not less than the highest price paid for the interest in shares so acquired. |

• | The board of directors of the offeree company must appoint a competent independent adviser whose advice on the financial terms of the offer must be made known to all the shareholders, together with the opinion of the board of directors of the offeree company. |

• | Special or favorable deals for selected shareholders are not permitted, except in certain circumstances where independent shareholder approval is given and the arrangements are regarded as fair and reasonable in the opinion of the financial adviser to the offeree. |

• | All shareholders must be given the same information. |

• | Each document published in connection with an offer by or on behalf of the offeror or offeree must state that the directors of the offeror or the offeree, as the case may be, accept responsibility for the information contained therein. |

• | Profit forecasts, quantified financial benefits statements and asset valuations must be made to specified standards and must be reported on by professional advisers. |

• | Misleading, inaccurate or unsubstantiated statements made in documents or to the media must be publicly corrected immediately. |

• | Actions during the course of an offer by the offeree company, which might frustrate the offer are generally prohibited unless shareholders approve these plans. Frustrating actions would include, for example, lengthening the notice period for directors under their service contract or agreeing to sell off material parts of the target group. |

• | Stringent and detailed requirements are laid down for the disclosure of dealings in relevant securities during an offer, including the prompt disclosure of positions and dealing in relevant securities by the parties to an offer and any person who is interested (directly or indirectly) in 1% or more of any class of relevant securities. |

• | Employees of both the offeror and the offeree company and the trustees of the offeree company’s pension scheme must be informed about an offer. In addition, the offeree company’s employee representatives and pension scheme trustees have the right to have a separate opinion on the effects of the offer on employment appended to the offeree board of directors’ circular or published on a website. |

• | under our articles of association to be effective upon completion of this offering, any resolution put to the vote of a general meeting must be decided exclusively on a poll. Under English law, it would be possible for our articles of association to be amended such that each shareholder present at a meeting has only one vote unless demand is made for a vote on a poll, in which case each holder gets one vote per share owned. Under U.S. law, each shareholder typically is entitled to one vote per share at all meetings; |

• | under English law, subject to certain exceptions and disapplications, each shareholder generally has preemptive rights to subscribe on a proportionate basis to any issuance of ordinary shares or rights to subscribe for, or to convert securities into, ordinary shares for cash. Under U.S. law, shareholders generally do not have preemptive rights unless specifically granted in the certificate of incorporation or otherwise; |

• | under English law and our articles of association, certain matters require the approval of 75% of the shareholders who vote (in person or by proxy) on the relevant resolution (or on a poll of shareholders representing 75% of the ordinary shares voting (in person or by proxy)), including amendments to the articles of association. This may make it more difficult for us to complete corporate transactions deemed advisable by our board of directors. Under U.S. law, generally only majority shareholder approval is required to amend the certificate of incorporation or to approve other significant transactions; |

• | in the United Kingdom, takeovers may be structured as takeover offers or as schemes of arrangement. Under English law, a bidder seeking to acquire us by means of a takeover offer would need to make an offer for all of our outstanding ordinary shares/ADSs. If acceptances are not received for 90% or more of the ordinary shares/ADSs under the offer, under English law, the bidder cannot complete a “squeeze out” to obtain 100% control of us. Accordingly, acceptances of 90% of our outstanding ordinary shares/ADSs will likely be a condition in any takeover offer to acquire us, not 50% as is more common in tender offers for corporations organized under Delaware law. By contrast, a scheme of arrangement, the successful completion of which would result in a bidder obtaining 100% control of us, requires the approval of a majority of shareholders voting at the meeting and representing 75% of the ordinary shares voting for approval; |

• | under English law and our articles of association, shareholders and other persons whom we know or have reasonable cause to believe are, or have been, interested in our shares may be required to disclose information regarding their interests in our shares upon our request, and the failure to provide the required information could result in the loss or restriction of rights attaching to the shares, including prohibitions on certain transfers of the shares, withholding of dividends and loss of voting rights. Comparable provisions generally do not exist under U.S. law; and |

• | the quorum requirement for a shareholders’ meeting is a minimum of two shareholders entitled to vote at the meeting and present in person or by proxy or, in the case of a shareholder which is a corporation, represented by a duly authorized representative. Under U.S. law, a majority of the shares eligible to vote must generally be present (in person or by proxy) at a shareholders’ meeting in order to constitute a quorum. The minimum number of shares required for a quorum can be reduced pursuant to a provision in a company’s certificate of incorporation or bylaws, but typically not below one-third of the shares entitled to vote at the meeting. |

• | the initiation, timing, progress and results of our current and future preclinical studies and clinical trials and related preparatory work and the period during which the results of the trials will become available, as well as our research and development programs; |

• | our estimates regarding expenses, future revenue, capital requirements and needs for additional financing; |

• | our expectations regarding timing of regulatory filings for, or our ability to obtain regulatory approval of, tebentafusp or any of our other product candidates; |

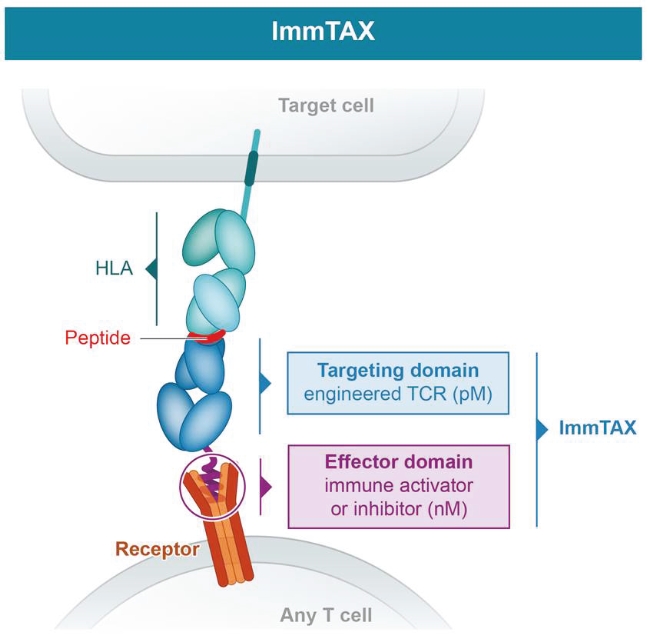

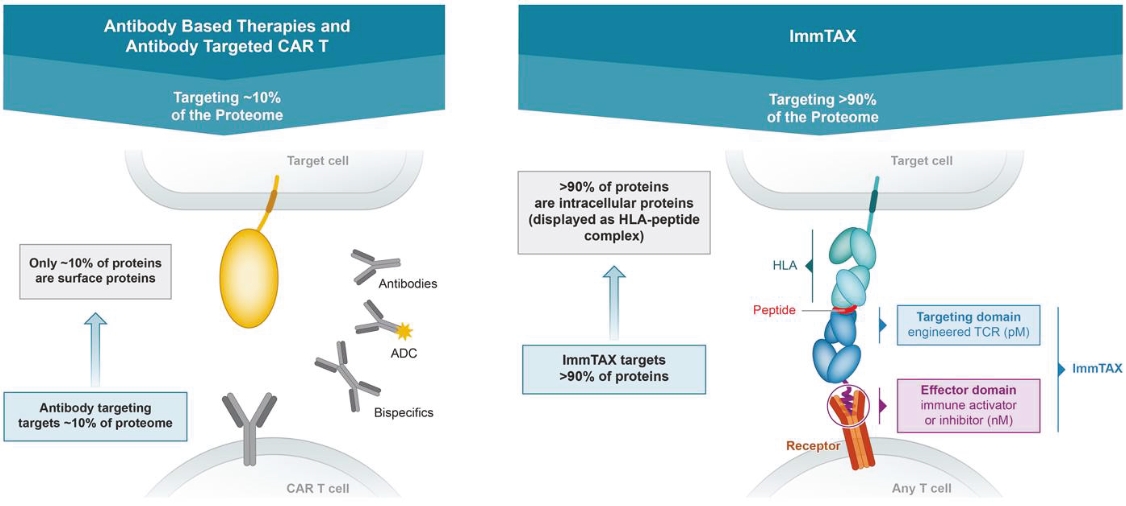

• | our ability to identify and develop additional product candidates using our ImmTAX platform; |

• | business disruptions affecting the initiation, patient enrollment, development and operation of our clinical trials, including a public health emergency, such as the ongoing the coronavirus 2019, or COVID-19, pandemic; |

• | the potential benefits of our product candidates; |

• | our expectations regarding the potential commercialization of, the potential market size and the rate and degree of market acceptance for any product candidates that we develop; |

• | our business strategies and goals; |

• | our plans to collaborate, or statements regarding our current collaborations; |

• | our ability to find future partners and collaborators; |

• | the performance of our third-party suppliers and manufacturers, |

• | our expectations regarding our ability to obtain, maintain and enforce intellectual property protection for our product candidates and our ability to operate our business without infringing, misappropriating or otherwise violating the intellectual property rights of others; |

• | the effects of competition with respect to tebentafusp or any of our other current or future product candidates, as well as innovations by current and future competitors in our industry; |

• | our financial performance and our ability to effectively manage our anticipated growth; |

• | our ability to identify, recruit and retain key personnel; and |

• | our expectations regarding the uses of the proceeds from this offering and the sufficiency of such net proceeds together with our existing cash and cash equivalents to fund our operations and capital expenditures. |

• | approximately $100 million to fund tebentafusp, our lead ImmTAC, for the treatment of metastatic uveal melanoma through the completion of our Phase 3 clinical trial as well as preparations for a commercial launch; |

• | approximately $20.0 million to advance the clinical development of IMC-C103C targeting MAGE A4 for the treatment of solid tumors; |

• | approximately $20.0 million to advance the clinical development of IMC-F106C targeting PRAME for the treatment of solid tumors; |

• | approximately $10.0 million to advance the clinical development of IMC-I109V targeting a functional cure for chronic HBV; |

• | approximately $20.0 million to continue to advance our pre-clinical programs and invest in our ImmTAX platform to discover and develop novel therapeutics; and |

• | the remainder for working capital and general corporate purposes. |

• | an actual basis; |

• | a pro forma basis to give effect to (i) the issuance and sale of 823,719 Series C preferred shares for aggregate gross proceeds of $75.0 million in December 2020; (ii) the borrowing of $50.0 million in November 2020 under a new debt facility with Oxford Finance Luxembourg S.A.R.L., or Oxford Finance; and (iii) our corporate reorganization; and |

• | a pro forma as adjusted basis to give further effect to (i) the sale of 8,333,333 ADSs in this offering at an assumed initial public offering price of $24.00 per ADS, which is the midpoint of the price range set forth on the cover page of this prospectus, and after deducting the underwriting discounts and commissions and estimated offering expenses payable by us; and (ii) the issuance and sale by us in the concurrent private placement of $15.0 million of our ADSs, or an estimated 625,000 ADSs based on the assumed initial public offering price, to the Bill & Melinda Gates Foundation. |

| | | As of September 30, 2020 | ||||||||||

| | | Actual £ | | | Actual $(1) | | | Pro Forma | | | Pro Forma As Adjusted | |

| | | (in thousands except share and per share amounts) | ||||||||||

Cash and cash equivalents | | | £56,687 | | | $73,245 | | | $198,245 | | | $394,845 |

Interest-bearing loans and borrowings | | | | | | | 50,000 | | | 50,000 | ||

Shareholders’ equity: | | | | | | | | | ||||

Series A preferred shares, nominal value £0.0001 per share, 1,699,576 shares issued and outstanding, actual; no shares issued and outstanding, pro forma and pro forma as adjusted | | | — | | | — | | | — | | | — |

Series B preferred shares, nominal value £0.0001 per share, 1,148,703 shares issued and outstanding, actual; no shares issued and outstanding, pro forma and pro forma as adjusted | | | — | | | — | | | — | | | — |

Series C preferred shares, nominal value £0.0001 per share, 823,719 shares issued and outstanding, actual; no shares issued and outstanding, pro forma and pro forma as adjusted | | | — | | | — | | | — | | | — |

G shares, nominal value £0.0001 per share, 62,750 shares issued and outstanding, actual; no shares issued and outstanding, pro forma and pro forma as adjusted | | | — | | | — | | | — | | | — |

Voting ordinary shares, 2,551,624 shares issued and outstanding, actual; 2,551,624 shares issued and outstanding, pro forma; shares authorized, shares issued and outstanding, pro forma as adjusted | | | 1 | | | 1 | | | 3 | | | 4 |

Non-voting ordinary shares, nominal value £0.0001 per share, 831,628 shares issued and outstanding, actual; no shares issued and outstanding, pro forma and pro forma as adjusted | | | — | | | — | | | — | | | — |

Additional paid-in capital | | | 330,390 | | | 426,897 | | | 501,893 | | | 698,493 |

Other reserves | | | 16,146 | | | 20,863 | | | 20,863 | | | 20,863 |

Accumulated deficit | | | (330,989) | | | (427,671) | | | (427,671) | | | (427,671) |

Total shareholders’ equity | | | 15,548 | | | 20,090 | | | 95,089 | | | 291,689 |

Total capitalization | | | £15,548 | | | $20,090 | | | $145,089 | | | $341,689 |

(1) | Translated solely for convenience of the reader into U.S. dollars at the rate of £1.00 to $1.2921, which was the noon buying rate of the Federal Reserve Bank of New York on September 30, 2020. |

• | 832,904 ordinary shares issuable upon the exercise of options outstanding under our existing equity incentive plans as of September 30, 2020, with a weighted-average exercise price of £63.23 per share; and |

• | 5,706,279 ordinary shares reserved for future issuance under our 2021 EIP which will become effective in connection with this offering, as well as any automatic annual increases in the number of ordinary shares reserved for future issuance under the 2021 EIP, as more fully described in the section titled “Management—Equity Incentive Plans;” and |

• | 4,014,267 ordinary shares (assuming an initial public offering price of $24.00 per ADS, which is the midpoint of the price range set forth on the cover page of this prospectus) underlying the grants to be issued prior to the closing of this offering to certain of our officers, directors and employees under our 2021 EIP, contingent and effective upon the execution and delivery of the underwriting agreement relating to this offering, with an exercise price that is equal to or greater than the price per ADS at which our ADSs are first sold to the public in this offering. |

Assumed initial public offering price per ADS | | | | | $24.00 | |

Historical net tangible book value per ADS as of September 30, 2020 | | | $3.68 | | | |

Decrease in net tangible book value per ADS attributable to our corporate reorganization and Series C preferred share issuance | | | (0.69) | | | |

Pro forma net tangible book value per ADS as of September 30, 2020 | | | 2.99 | | | |

Increase in net tangible book value per ADS attributable to this offering and concurrent private placement | | | 4.17 | | | |

Pro forma as adjusted net tangible book value per ADS after this offering and concurrent private placement | | | | | 7.16 | |

Dilution in as adjusted net tangible book value per ADS to new investors participating in this offering | | | | | $16.84 |

| | | Ordinary Shares or ADSs Purchased | | | Total Consideration | | | Average Price Per Ordinary Share | | | Average Price Per ADS | |||||||

| | | Number | | | Percent | | | Amount | | | Percent | | | | | |||

Existing shareholders | | | 31,782,885 | | | 79.2% | | | $330,391,000 | | | 62.3% | | | $10.40 | | | $10.40 |

New investors | | | 8,333,333 | | | 20.8% | | | $200,000,000 | | | 37.7% | | | $24.00 | | | $24.00 |

Totals | | | 40,116,218 | | | 100.0% | | | $530,391,000 | | | 100.0% | | | $13.22 | | | $13.22 |

• | 832,904 ordinary shares issuable upon the exercise of options outstanding under our existing equity incentive plans as of September 30, 2020, with a weighted-average exercise price of £63.23 per share; and |

• | 5,706,279 ordinary shares reserved for future issuance under our 2021 EIP which will become effective in connection with this offering, as well as any automatic annual increases in the number of ordinary shares reserved for future issuance under the 2021 EIP, as more fully described in the section titled “Management—Equity Incentive Plans;” and |

• | 4,014,267 ordinary shares (assuming an initial public offering price of $24.00 per ADS, which is the midpoint of the price range set forth on the cover page of this prospectus) underlying the grants to be issued prior to the closing of this offering to certain of our officers, directors and employees under our 2021 EIP, contingent and effective upon the execution and delivery of the underwriting agreement relating to this offering, with an exercise price that is equal to or greater than the price per ADS at which our ADSs are first sold to the public in this offering. |

| | | For the nine-month period ended September 30, | | | For the years ended December 31, | |||||||

| | | 2020 | | | 2019 | | | 2019 | | | 2018 | |

| | | (pounds sterling, in thousands, except for share and per share data) | | | (pounds sterling, in thousands, except for share and per share data) | |||||||

Consolidated statement of loss and other comprehensive income data: | | | | | | | | | ||||

Revenue | | | 22,694 | | | 20,027 | | | 25,669 | | | 23,654 |

Other operating income | | | 408 | | | 420 | | | 185 | | | 622 |

Operating expenses: | | | | | | | | | ||||

Research and development | | | (57,566) | | | (75,415) | | | (99,991) | | | (83,575) |

Administrative expenses | | | (31,569) | | | (35,611) | | | (44,183) | | | (34,156) |

Operating loss | | | (66,033) | | | (90,579) | | | (118,320) | | | (93,455) |

Other income | | | — | | | — | | | — | | | 4,979 |

Finance income | | | 1,972 | | | 1,134 | | | 1,510 | | | 1,140 |

Finance costs | | | (2,272) | | | (6,532) | | | (9,379) | | | (842) |

Non-operating (expense) / income | | | (300) | | | (5,398) | | | (7,869) | | | 5,277 |